Botswana’s Minerals Legal & Institutional Frameworks

Can Botswana keep up its reputation?

– Sheila Khama July 2023

Introduction

This is the first of four articles on Botswana’s diamond mining industry. My commentary focuses on the country’s main law governing mineral development as it relates to arrangements between the Government and De Beers Group. I provide an overview of Botswana’s legal and institutional structures and sequential highlights of the legal aspects of the partnership arrangements. Drawing upon accepted governance principles and sustainable development standards, I comment on what I believe works and does not work. In doing so, I am biased towards interests of the State and the interests of citizens of Botswana.

Background

The foundation of the relationship between Botswana and De Beers is the country’s mining law through which the Government is custodian of mineral wealth. An important governance principle is that successive administrations act only in the interest of citizens and not the political party that happens to be in office. This is an essential legal and moral obligation that gives rise to the notion of a fiduciary role. A fiduciary is an entity or a person to whom property or power is entrusted for the benefit of another.

There are several factors that make a relationship a fiduciary one, and three are especially relevant in this case.

- The beneficiary has delegated authority to the fiduciary to act on its behalf;

- the fiduciary has discretionary powers over the beneficiary’s assets or interests, and

- the fiduciary is in a position superior to that of the beneficiary due to specialized access, knowledge or ability. In the case of an elected government and civil servants, all factors are indicative of the onerous nature of the task and the legitimate expectation by the public of those responsible to exercise a heighted sense of duty when administering matters relating to Botswana’s mineral wealth.

Given the finite nature of mineral resources, a second guiding principle for those responsible for developing Botswana’s mineral wealth is the concept of sustainable development. This requires that national policies on mineral development be formulated to ensure that the Government and others involved in oversight of mineral exploitation do so in ways that meet the needs of the current generation but without compromising the needs of future generations. An essential point of reference for meeting this standard is a responsive economic, social, and environmental stewardship, which is also the embodiment of Environment Social and Governance (ESG) frameworks. To a large degree, my commentary is guided by these governance and sustainable development concepts, principles, and standards.

Attracting Investment in Mining

The value of a country’s mineral wealth is latent, and to manifest it, it must be unlocked. Ensuring that this value is unlocked is an integral part of the Government’s performance of its legal responsibility as custodian of mineral resources. To achieve this, the Botswana Parliament enacted several laws but only approved a minerals policy in 2022. Until then, the Government operated on a set of principles. The 2022 Minerals Policy contains objectives, aims and core pillars. However, many essential laws were enacted soon after self- rule in 1966. Among other things, the laws regulate mineral exploration, mining operations, water access, land access, environment impacts, employee rights, community rights and taxation. These laws and relevant national institutions are the tools the Government deploys to unlock and enhance the economic value of mineral wealth. The laws are also the means by which Government institutions perform routine oversight of the activities of those involved in exploration, mining, and other activities in the value chain. The most important law through which the Botswana Government performs its responsibilities, protects its legal rights, and exercises authority in upstream activities is the Mines and Minerals Act of 1999 (the original Mines and Minerals Act of 1967 was replaced by the Mines and Minerals Act of 1977, which in turn was replaced by the current Act). For comparison with all other African countries, the Africa Legislation Atlas is a reliable source – (www.a_mla.org; https://bgi.org.bw/sites/default/files/Botswana%20Minerals%20Policy%20 2022.pdf).

To give effect to the policy and laws, starting at the exploration phase, the Government grants mining companies the right to search for minerals. At this stage, the goal is to entice companies by giving them exclusive rights to search for a specific mineral in a specific area in the hope that the company will make a discovery. Annual exploration fees per square kilometre are nominal. While the fee for a license is insignificant, investing in mineral exploration takes time, is costly and risky – (https://www.bgi.org.bw/). In Botswana, diamond exploration was carried out on and off during and after the colonial era before any discovery was made. Diamond discoveries are particularly rare, and it is estimated that only 2% of all rock that hosts diamonds have enough quantity to financially justify development. It is therefore not surprising that since the discovery of the Kimberly diamond pipe in 1867, the world’s next significant discovery was 99 years later in Botswana. However, companies take the risk in the hope that a single discovery will make up for years of financial losses.

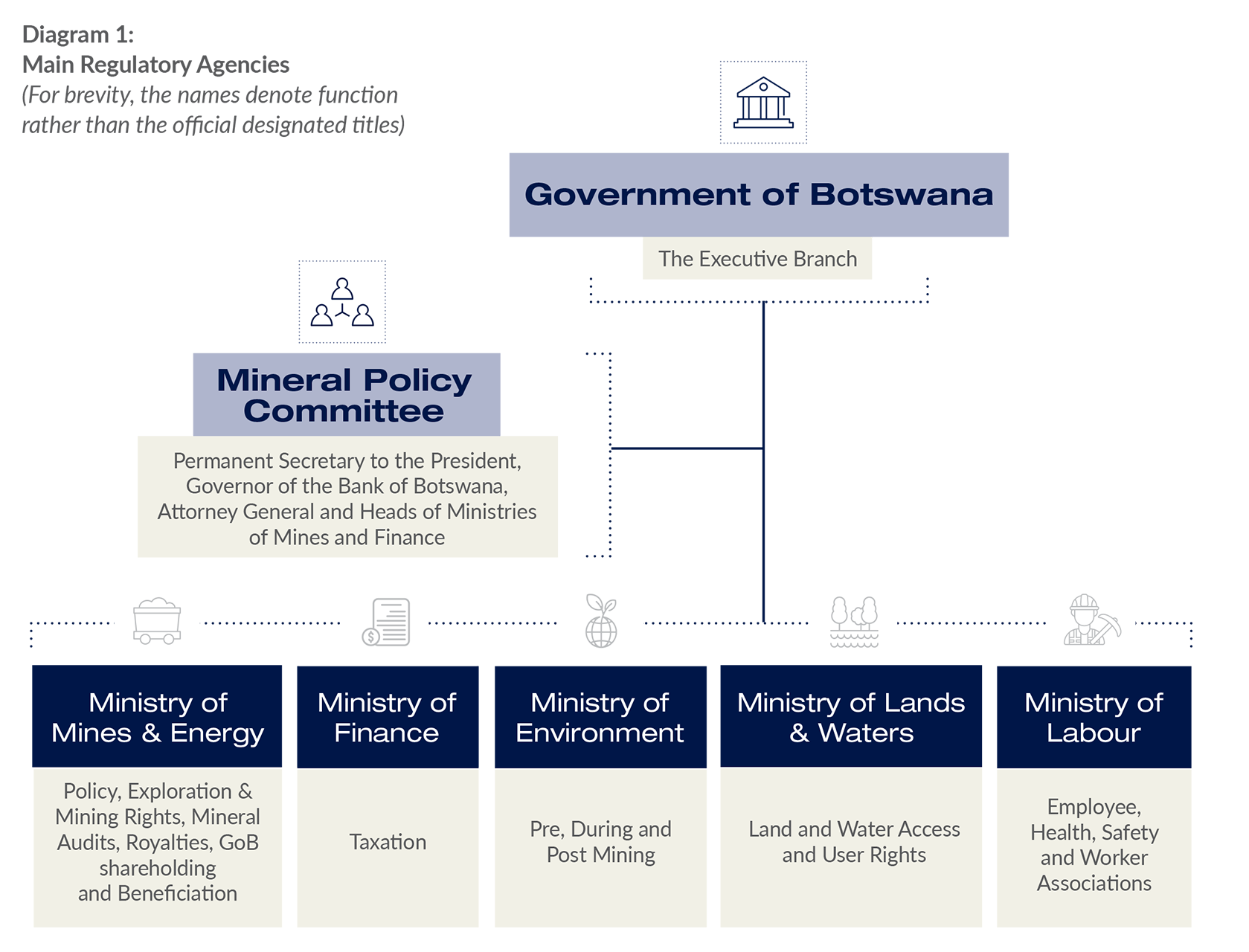

As a result of the laws, numerous public agencies were established to be responsible for implementation. Diagram 1 illustrates the main ones in Botswana. An important arm for the strategic and oversight work of government is an ex officio body known as the Minerals Policy Committee (MPC). According to the 2022 Minerals Policy, its mandate is to ‘provide strategic direction for minerals development at high and national level.’ This team is made up of senior public officials (see Diagram 1). Institutionally, the MPC has also been responsible for negotiating mineral development and marketing arrangements with investors across all minerals

An important feature of the laws governing mineral exploitation is the rights and privileges accorded to the Government and to investors. In the paragraphs below, starting with entitlements to the Government, I summarize those rights and privileges that are specifically pertinent to the relationship between the citizens of Botswana (Botswana) and De Beers.

Government Entitlements

As the owner of the mineral deposit, the Government naturally ranks higher than the companies that make the discoveries and ultimately develop the mines. Thus, the Government enjoys many rights and privileges beyond those assigned to investors. It is not my aim to reference every one of these rights, instead, I have selected a few that I believe are material and indicative of the Government’s position of superiority. I am biased towards those that relate directly to the Government’s custodial role and to its responsibility to citizens in relation to its partnership with investors.

Unfettered Information Access

Aspects of the bankable feasibility study are required by law, but the study is conducted and financed by the company as project sponsors. The company uses the findings of the study as the main project document to raise finance for the development of the mineral deposit. The study is extensive and produces volumes of reports covering different scopes of work necessary to inform investment decisions and project design. The study covers proposed environmental impacts, infrastructure needs and engineering design, cost estimates, medium-term market conditions and perceived degree of profitability or lack thereof. It enables the Government to take a view on appropriate levels of tax, royalty, and equity. Investors rely on the study to assess the project’s economic potential, risks, and rewards. The Government relies on the reports to validate (or dispute) investor assumptions and conclusions. In the case of diamonds, once validated, the reports are the basis for negotiating terms for licensing, marketing, and other development arrangements. They include but are not limited to the rate of exploitation, royalty, taxation, and Government equity.

Government Equity

In this context, equity is the level and not the value of an investor’s stake in a company. From an investment perspective, the most important provision in Botswana’s mineral law is the Government’s right to acquire equity in any company formed for purposes of mining a mineral deposit. At the time of granting the license, the Government is at liberty to exercise this right up to 15% equity by law or to negotiate a higher share of equity. In some cases, the Government elects to forfeit this right. In the case of the Orapa/Letlhakane discoveries, Botswana exercised the country’s legal right and acquired 15% carried interest. That is the right to automatic allotment of shares in the mining company without Botswana making an upfront financial contribution while the investors did.

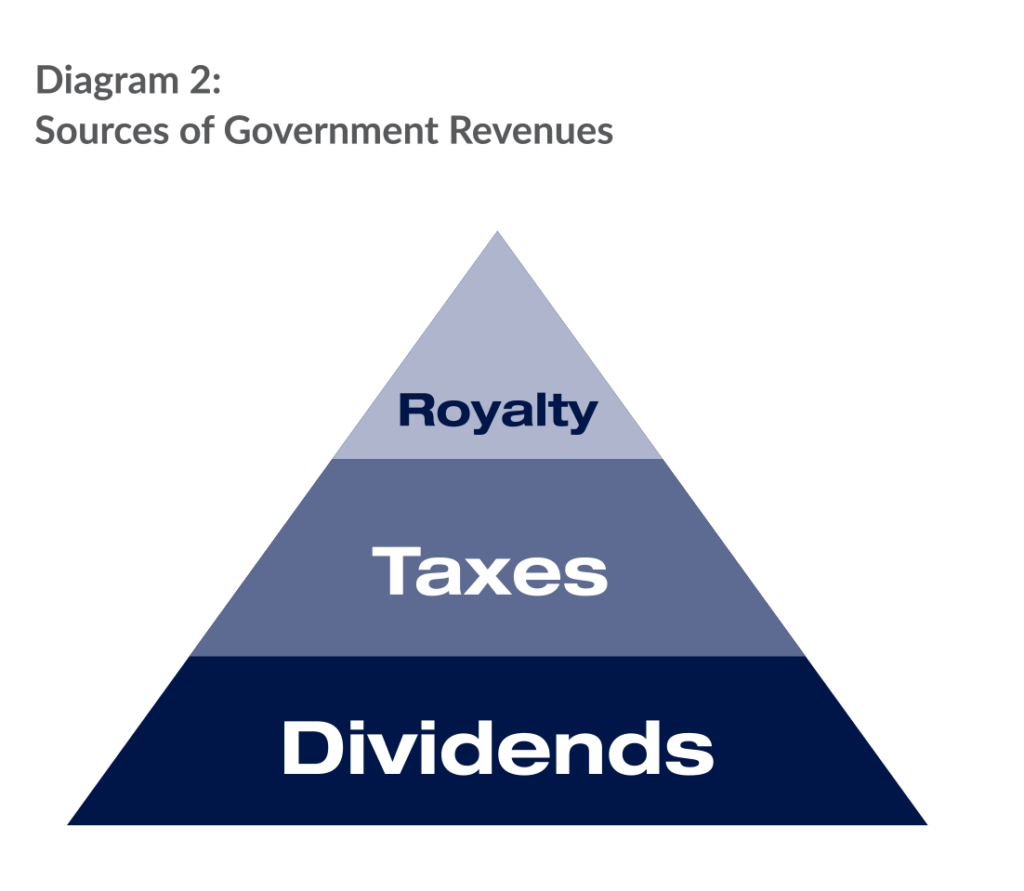

The ratio of equity does not mirror the ratio of financial benefits, and the latter should not be misconstrued to entitle the JV partners to an equal share. This is because based on Botswana laws, the Government’s entitlements exceed and rank superior to those of the investor. First, the Government levies rent (otherwise known as royalty payments) on the company that is mining the diamonds (and not De Beers). Royalty is nonnegotiable and is paid to compensate Botswana for Debswana’s rights to extract the country’s minerals, regardless of whether the company is profitable. Royalty is based on perception of the value of minerals. The rate for diamonds is 10%, and much higher than that of other minerals, which is only 3%. The 3% rate is more aligned to rates in many parts of the world, but Botswana took the view that the economics of the deposit justified a higher rate. The Government also imposes corporate tax (and other less onerous forms of tax) on the same company as provided for in national laws. Finally, as one of the shareholders, whenever the company declares dividends, the Government receives payment in accordance with its 50% equity. Dividends are income distributed to shareholders from profits. Not included in payments to the Government are annual rentals for surface rights, which are paid to the land authorities. Diagram 2 shows the hierarchy of payments to the Government by Debswana and other mining companies unless for whatever reason the Government decides to set aside any of the taxes which is not the case for the JV with De Beers

Financial Payments

Shareholder Rights

In addition to its position as the regulator with unfettered access to mine operations, through representatives on boards of companies the Government also has additional and unfettered access to all information relating to the affairs of Debswana. The Government routinely receives company financial and non-financial reports through the board and subcommittees and can also demand more if it chooses. If necessary, the Government has the power to investigate and generate reports for itself and in keeping with its own needs. In exercise of this authority, in 2003 the Government, through the Attorney General’s Chambers, commissioned a UK firm called Control Risk to conduct a financial forensic audit of the operations of the Debswana JV in its capacity as a regulator and not as a JV partner. The audit concluded that the company was fully compliant with the country’s laws. The gesture was an example of protection of public interest that could be extended to other mining companies.

Environmental Protection

Botswana laws not only require Environmental Impact Assessment Studies (EIAS) at project stage, but also annual environmental protection plans, reports, and site inspections. Other Government entitlements include mineral audits, corporate tax audits, employment of citizens and procurement from citizen companies where appropriate.

These examples are indicative of frameworks that empower the Government to protect national interests and only if the powers vested in the authorities are not exercised would the Botswana public be exposed to risk. A second and important caveat is that, established institutional checks and balances between the three arms of government being, the Executive Branch, Parliament and the Judiciary are resourced to be robust and to perform their stated governance responsibilities unobstructed.

De Beers Entitlements

Investor Equity

Mineral exploration is akin to research and development (R&D), and companies take a calculated financial risk when searching for minerals. If the company has operations in different jurisdictions, it centralizes its exploitation activities and deploys them to benefit from economies of scale by adopting a global rather than a disjointed approach. The company’s technology and skills are managed centrally and deployed strategically based on perceived prospects. The results are potential maximum rewards and minimum risk. In 1955, in his capacity as the Chairperson of De Beers Consolidated and Anglo American Corporation of South Africa, Harry Oppenheimer and his executive team believed that these prospects were greatest in Botswana, and they concentrated a significant amount of the company’s resources to resume a search for diamonds that went back to decades earlier. The effort paid off and under Botswana mineral law, the company’s rights are protected such that having made the Orapa/Letlhakane discovery, it earned the right to develop the mine alone or in partnership with the Government (if the Government chose).

Mindful of the risk taken by investors and desirous of attracting foreign direct investment (FDI), Botswana’s mineral policy, exploration mineral development and tax laws are designed to protect investors’ rights to recoup a fair return. A pre-condition is protection of the Government’s own rights to benefit from its mineral wealth. The mining company (in this case initially De Beers but latter Debswana) also has the right to sell the minerals in order to recoup costs from the initial and subsequent investments. This afforded De Beers and all other mining companies the right of first refusal in relation to the company’s discoveries and sale of mineral production. For mining companies, security of tenure through protection of property and mining rights, based on a stable mining regime, and the ability to sell the product are two of the most important considerations for making the original investment in the development of a mine. Thus, from the start, these rights would have been of prime consideration by De Beers. However, the Government did not relinquish ownership of the resource to the investor. Instead, the development is carried out on terms negotiated between De Beers and the Government as the representative of Botswana citizens. In this respect Botswana is not unique and mirrors laws in many other parts of the African continent.

Financial Benefits

In addition to the right to develop the mine (in the context of the discoveries above), by law De Beers was entitled to financial benefits, specifically through cost recovery arrangements and a 50% share of any dividends paid. Hence, as Former President Mogae said in 2009 at the African Development Bank, ‘additionally, and in recognition of the right of the investor to recoup investment, it was also agreed that the marketing agreement would be renegotiated every five years.’ In the same speech, he said, ‘in return the government accepted the single channel marketing that is to sell only through the De Beers Central Selling Organization now known as the Diamond Trading Company.’ Commission from the Sales Agreement provided De Beers with an additional source of income necessary to balance financial benefits. The arrangement also incentivizes the company to secure as high a price as possible for Debswana diamonds because De Beers gains financially from the high prices, and it has everything to lose from low prices. This arrangement continues today, and after interim negotiations of the Sales Agreement, the split of distributable payments from Debswana stands at 80.8 cents on the dollar in favour of the Government. An additional and important factor that explains the higher than usual Government share is the highly profitable nature of Botswana’s Jwaneng mine. Therefore, the ratio of revenue should be understood in the specific context of the economics of these diamond deposits. Indeed, with time the deposit will diminish, and the ratio will need to be adjusted to ensure the distributable financial benefits between the two Debswana JV partners remains equitable.

Continuous Mine Investments

Just as it was necessary to invest in infrastructure and other resources to commission and decommission a mine, in order to continue mining the resource, investments must continuously be made, and capital injected to extend the productive life of a mine. The nature and degree of the financial commitment is driven by several factors, the most important of which are the geology of the deposit and the stage in the life cycle of a mine. Generally, the older the mine becomes, the higher the cost relative to the revenue generated. Equally, moving from open-pit operations to underground operations calls for much higher financial commitment, and the decision to switch from open-pit to underground operation is as much a mining engineering and geotechnical decision as it is an economic one. Because of this, De Beers and Botswana have previously invested in the mines and will have to continue to plough profits back into the development of the mines.

In recognition of this, Botswana laws protect the right of De Beers to recoup the cost associated with the company’s contribution to subsequent investments. As an example, development costs for the cut 9 projects at Jwaneng which extends the life of the mine till 2035 will cost Debswana shareholders about US$2b. Runner-up: Excellence in Diamonds – Debswana’s Jwaneng (miningreview.com). It is expected that the project costs for taking the same mine underground will be even higher. Among other considerations, Botswana is a favoured destination because the country’s law guarantee the investor security of tenure from the prospecting stage through to mine development and renewal of mining licenses. Botswana has been fully compliant with its own laws, but were the laws ignored, the Government would risk disincentivizing De Beers and would therefore put continuation of the mining operations at risk due to lack of investment. Commitment by the investors is premised on the expectation that for both parties, the entitlements remain protected in law – (Botswana ranks most attractive for investment in mining – Weekend Post).

A sudden or incremental erosion of these entitlements by the Government unsettles investors and their financiers. Development partner institutions and sovereign risk rating firms take a dim view of any tendency for countries to infringe upon the rights of investors. The business environment becomes unstable and is seen as akin to resource nationalism (the propensity for governments to exercise greater control over capital than can reasonably be justified from an ownership and a free-market economy perspective). However, companies also see sudden changes in legislation as akin to negotiating in bad faith. For their part, governments often view a change in legal and fiscal policies as making up for imbalances in the original deals between themselves and investors, and changes are therefore commonplace in many jurisdictions. Importantly, the right of governments to periodically amend policies and laws to meet national development needs is an essential custodial function that cannot and should not be subjected to the whims of investors. The challenge is in how to strike the right balance between the two interests.

What Has Worked

Continuous Mine Investments

On matters of the law, institutional frameworks and regulatory instruments, Government’s oversight of the activities of De Beers and Debswana has been effective in several noteworthy ways. Some of these are discussed below.

Consistent Application of the Law

Historically, Botswana’s regulatory environment has been stable and lauded for its respect for the rights of all parties including in governance terms in which Botswana’s performance over 40 years has been enviable. In addition to the guarantee of rights cited in the preceding paragraphs, Botswana’s ability to attract investors based on availability of geological data, consistency in the content and application of the law and exclusion of discretionary powers has been cited by mining companies as proof of the country’s competitiveness. The result is favourable ratings by international watchdogs. In regulatory terms, Botswana is perceived as a good destination by mining companies surveyed by the Frasers Institute Mining Survey – (https://www.fraserinstitute. org/studies/annual-survey-of-mining-companies-2022). According to the Survey Botswana was rated top in Africa and on par with others elsewhere including Western Australia for attractiveness as a destination for mineral exploration based on regulatory effectiveness.

Through the outcomes of the 2023 negotiations for the renewal of the mining licenses for the Debswana mines, Botswana’s regulatory consistency has manifested once again proving that on application of the law and therefore guarantee of investor security of tenure, Botswana is indeed a worthy mining destination. The mining licenses for the four lease areas only expire in 2029 and pragmatically but consistent with Botswana’s mining law, principle agreement has already been reached to extend the Debswana mining licenses for another 25 years effective from 2029. This means the decision to renew the license was brought forward by 6 years and will be valid up to 2054. The decision paves the way for investment in the Jwaneng resource extension and mine infrastructure projects. The subtlety cannot be lost on De Beers and other investors that Botswana remains open for business. The decision also speaks to the entrepreneurial mindedness of the Botswana Government which no doubt realizes that failure to extend the license would disrupt operations especially as relates to future production and income. It would also have implication on the very future of the Debswana partnership.

Mineral Resources Management

As protector of public interest, knowledge of a country’s mineral wealth and the economics of each deposit is the foundation for the Government’s custodial duty. To leverage the resources through equity, royalty payments, production sharing, tax, value-addition and other channels, this knowledge is indispensable, because otherwise the Government negotiates, regulates and plans in a vacuum. So, this knowledge is so vital that while other skills can be outsourced without compromising national interests, it is inconceivable that the Government could outsource this capability and still effectively perform its custodial duty. In this case, all indications are that Botswana has adequately invested in systems for short- and long-term mineral resources development planning and management. Through the Department of Mines, the Government receives routine reports on resource estimates, mining plans, production returns, export data and revenue estimates. For diamonds, the Government employs an independent mineral valuator to assess Debswana diamonds before sale and export. unless the company’s figures and those of the Government’s independent valuator reconcile, the sale of goods by Debswana to De Beers cannot be finalized nor export approved.

Independence of Civil Servants

An important part of the institutional arrangements has traditionally been the separation of political roles from the day-to-day work and authority of senior civil servants. This is because administrative heads of ministries are appointed centrally by the Permanent Secretary to the President and report to her or him and not to the ministers whose portfolio they may fall under. Thus, the appointment of heads has not followed the political electoral cycle. To the degree that there is an oversight committee of Parliament relating to the work of a ministry, its head of ministry reports directly to that committee and not the minister. Over the years, this independence of Botswana civil servants based on exclusion of the power of the minister over their careers has rendered technocrats less vulnerable to political interference. In governance terms, this principle should be sacrosanct in order to effectively steward mineral development through avoidance of conflict of interest, evelopment of manpower and building of institutional capacity.

Diamond Jewellry Consumer Confidence

Protection of Intellectual Property (IP)

At mining, sorting and valuing stages, De Beers continuously innovates to gain advantage over its competitors and has generated significant value for itself and the JV. Much of the technology is deployed in the Botswana operations to increase efficiency and revenue for both. A diamond industry analyst, Richard Chetwode writes ‘the only diamond company to spend millions on R&D to defend the ‘integrity’ of natural diamonds… the list seems to go on and on, but all of these benefit Botswana.’ – (https://bne.eu/comment-the-diamond-industry-isin-crisis-and-botswana-is-going-rogue-279616/). Botswana’s legal protection of IP rights against infringements should not be taken for granted. Availability of laws on IP protection in line with the international norm are essential to give assurance to De Beers for deploying the technology without risk to the company.

Public Participation in Policy and Law

Botswana has conducted systematic grassroots studies on matters of communal land-tenure systems as well as on mineral policy and law. The revision of the mining law and fiscal regime that culminated in the enactment of the Mines and Minerals Act of 1999 provided consultations with all the District Councils in Botswana. What remains to be confirmed is how well the country has done as a result of this new Act. For instance, how much progress has been made regarding citizen participation and local procurement of goods and services?

What COULD BE IMPROVED

Conflicting Interest Between Regulatory and Investment Arms

From a mining and a tax collection perspective, the responsibilities of the Government as the regulator and an investor in Debswana overlap. The Ministry of Mineral Resources and Energy is not only the shareholder representative but is also the regulator of many of the company’s activities and is part of the Government’s negotiation teams. Through the relevant departments and as the assessor and receiver of tax revenue, the Ministry of Finance has performed similarly overlapping roles as well, but to a lesser extent. Looked at optimistically, this might be perceived as stabilizing the environment, ensuring continuity and consistency. It might also be seen as ensuring that those officials who negotiate with De Beers also own the outcomes because through regulatory oversight and seats on corporate boards, the officials oversee implementation of agreements and have a vested interest in their success. The counterargument might be that too much power and knowledge is concentrated in the hands of a few. From a governance perspective, the institutional arrangements create two challenges. The first is the lack of checks and balances between government agencies responsible for investment and those responsible for regulating the activities of investors, including Debswana. The second is the inherent conflict that faces representatives who are also regulators but must collaborate with De Beers to ensure the commercial performance of Debswana. Admittedly, De Beers’ representatives face the same challenge regarding interests and potential bias when dealing with the subsidiary rather than the De Beers Group commercial interests. The difference is that as a private company, at Group or subsidiary level, De Beers’ single motivate is profit. However, in government circles, party political and national interest are not always reconcilable.

Mine Closure Remediation

The only certainty in mining is that the mine will reach a stage at which it will no longer be profitable to continue with mining (i.e., economic gain vs resource exhaustion). This suggests that simultaneous to oversight of routine mining operations, measures should be put in place to remediate the physical and social environment at mine decommissioning stag. If not, the country runs the risk that post-mining legacy costs become the Government’s burden. But Botswana has not yet enacted the necessary law (presently in draft form). If passed, the law would prevent this risk. Such laws not only require annual environmental protection plans, reports, and site inspections, but the law stipulates that the JV produce a comprehensive mine closure plan complete with cost estimates. It would also require the creation of a trust fund to meet such future costs and de-risk the matter.

De Beers and Ruling Party

The intimate relationship between the Botswana Democratic Party (BDP) as the ruling party for the past 53 years, and De Beers has been evidenced by funding the party and by granting personal loans to its leadership. Admittedly, since some transactions occurred 40 years ago, one might be lenient given that governance standards were less stringent globally. Nevertheless such a relationship epitomizes conflict of interest, flies in the face of reason given modern day governance trends and the need for accountability and transparency. Specifically, by inserting itself between the Government, the citizens of Botswana and De Beers, the ruling political party compromised the Executive Branch. The question is, did the party profit from the Government’s relationship with De Beers and vice versa at the expense of citizens? The answer is there is no verifiable proof one way or the other. But, unsurprisingly, this has undermined public trust because regardless of any change in party and corporate donations policy, current and future party members are beneficiaries of previous financial support by De Beers

Political Power

However, one thing has not changed. That is the national election victories by the same party for 50 years, albeit with the confirmation of regional and international election observers. This means that one political voice has presided over Botswana’s mineral affairs for half a century. Arguably, in the early days of the partnership, the continuity might have been deemed a source of stability. However, at this stage it is potentially problematic for several reasons.

At independence, so limited was Botswana’s human capital that estimates show that the country only had 40 university graduates. Due to the absence of meaningful public institutions and skilled personnel in 1969, negotiations between De Beers and Botswana were understandably in the hands of a few, notably the first President of the Republic, Sir Seretse Khama, and his Vice President, Sir Ketumile Masire, who personally negotiated with De Beers with the support of foreign experts. In time, Botswana established institutions and developed enough manpower to decentralize roles and responsibilities.

To begin with, in governance terms, it is not inclusive. The absence of voices of opposition parties undermines public participation by those parties and their voters on matters relating to the country’s most important economic asset. It undermines the necessary checks and balances that would be possible through periodic change of government. Thus, although the elections are legitimate, the one-sided nature of the political voice does not augur well for broad-based citizen participation on matters pertaining to the partnership with De Beers. Including parliament in the process would address the matter. Using Parliamentary records that (unlike Cabinet Meetings records) are made public, scholars would also subject the agreements to analysis, enriching public debate and potentially lay the foundation for future negotiation strategies.

Therefore, though legally compliant with the country’s laws, in governance terms, Botswana has fallen behind on matters of inclusion, accountability and transparency. What is the alternative? The experiences of countries like Norway in the oil sector as relates to the role of the Parliament and the Executive Branch, might offer an answer – (https://www.equinor. com/about-us/corporate-governance).

Public Participation in Negotiations and Agreements

The democratic system of government empowers those in power to be the voice of the electorate, but it does not substitute for citizens’ voices. While there is a case for negotiating out of public view, there are benefits in making the agreed terms publicly available after conclusion of the negotiations. In this respect, the failure by the Government to include parliamentarians in negotiations and on matters of mining in Botswana’s biggest asset defies logic. The private nature of details relating to the scope and content of agreements, such that parliamentarians, NGOs, and the public have no access to them, fails the basic test of transparency, accountability, and public participation. It goes against the democratic concept of Government of the people, by the people, for the people and leans towards a government of the party for the members.

Freedom of Information Law

Though not confined to the diamond industry, the absence of a freedom of information law in Botswana creates problems of transparency and permeates all economic policy but especially those relating to diamonds because of their far reaching long-term socio economic impacts. But this might change because the current administration made an electoral commitment to enact the law.

Conclusion

In mining policy and mineral economic development terms, the ruling party has performed well as a steward of Botswana’s diamond wealth. De Beers took a risk and invested hugely in exploration and enjoyed a stable environment and conducive relations for nearly half a century. Botswana’s image and track record of responsible use of mineral resources has strengthened consumer confidence. De Beers’ technology has helped unlock diamond wealth including the very discovery of the deposits. The partnership has been a driver of the national and corporate brand to their mutual benefit. As will be seen in the next blog in the series, year after year, both partners received a high return on the investment in Debswana. It seems sensible to build on this foundation.

Sorry, the comment form is closed at this time.